Once you complete your college education, it is advisable to venture into the world of investing. By investing wisely, you can potentially earn more money than you would through traditional work alone.

This concept is often summarized as “letting your money work for you,” even while you sleep. However, it is important to note that different phases of life require different investment strategies. In your younger years, you can afford to take higher risks in your investments. As you grow older, it becomes prudent to prioritize safer options.

Relying solely on a single source of income may not be sufficient for supporting yourself and your family, especially considering the rising inflation rate. To combat inflation effectively, it is inevitable to leverage the power of compounding. This involves reinvesting your earnings to achieve exponential growth.

To meet short-term goals, such as purchasing a car or building a house, it is essential to explore investment opportunities that offer rapid and substantial returns. Conversely, when saving for retirement, it becomes prudent to focus on low-risk investments that provide a steady income, particularly when other sources of income may diminish.

The smartest approach is to educate yourself about all three aspects—high-risk, low-risk, and medium-risk investments—and then create a portfolio with an appropriate allocation based on your risk appetite and goals.

In order to assist you in achieving your investment goals, we have conducted thorough research and compiled a list of investment options. This will enable you to make informed decisions about where we can invest money.

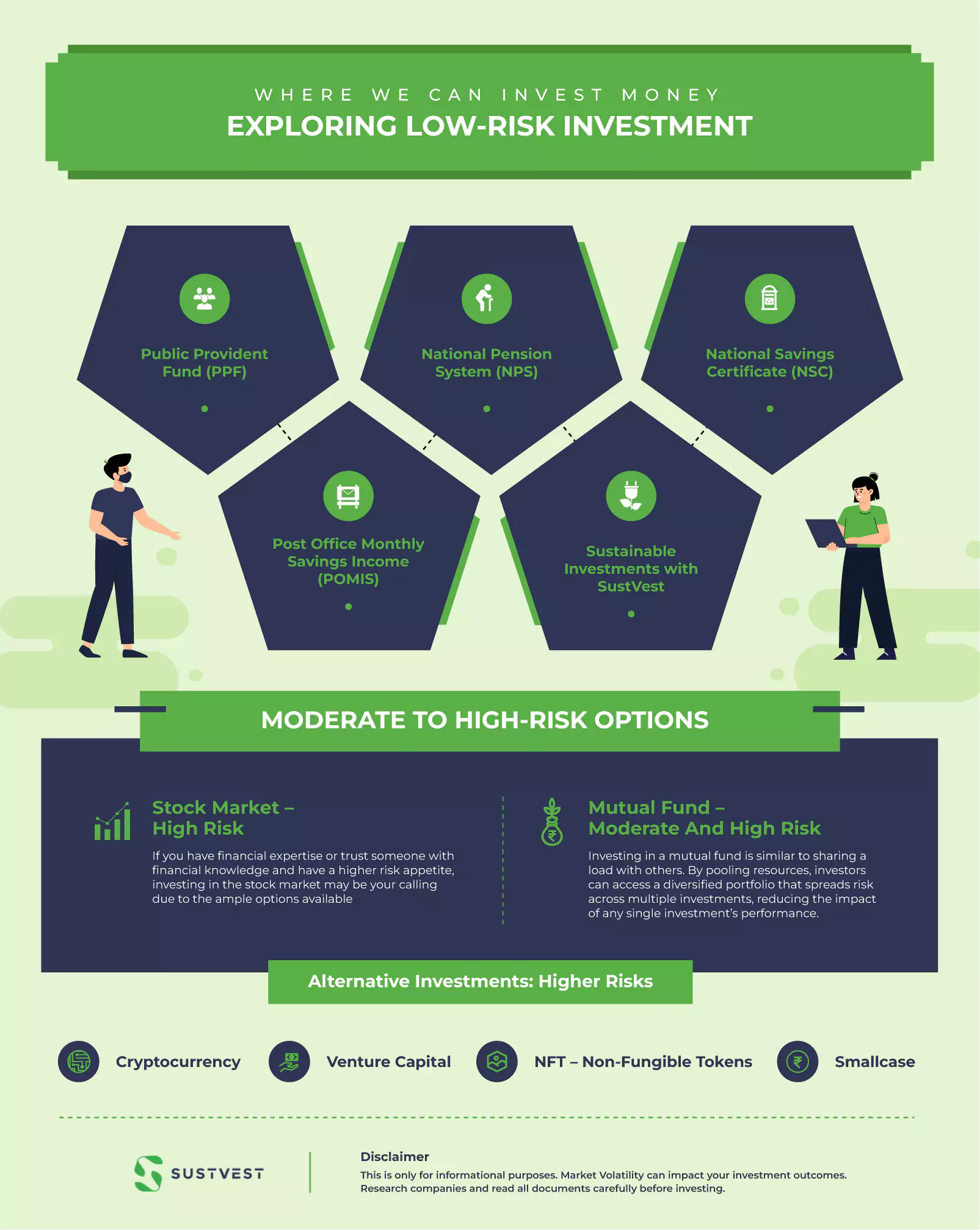

Where We Can Invest Money: Exploring Low-Risk Investment

Public Provident Fund (PPF)

If you prefer low volatility and safer returns, the Public Provident Fund (PPF) can serve as your safe haven. This government-backed savings scheme allows you to deposit your money for a period of 15 years, during which you can earn an interest rate ranging between 7% to 9%.

The minimum deposit amount for opening a PPF account is Rs. 500, while the maximum deposit limit is set at Rs. 1.50 lakh in a financial year. The PPF is particularly favored by traditional investors due to its ability to generate consistent returns while also offering completely tax-free interest earnings.

Its tax benefits make it an attractive choice for investors seeking a secure and tax-efficient investment option

National Pension System (NPS)

If you are looking for an investment option that saves your tax and generates steady returns during your retirement NPS should be your pick.

- NPS is a well-known government-backed retirement savings scheme.

- You can start with as low as 6,000 INR yearly and go as high as 200,000 INR.

- Even though it has a fixed lock-in period until the age of 60 for Tier 1, it allows for a few withdrawals.

- Under Section 80C, you can save up to 1.5 lahks INR as a tax exemption.

- For example, Mr. Malhar at the age of 30 starts investing 6000 per month till the age of 60, the total investment would be 21.3 lakh, and the interest earned would be 1.81 crore.

- If your investment goal is purely long term NPS is considered the best by financial gurus.

National Savings Certificate (NSC):

If you aim to earn higher returns than fixed deposits (FDs) while enjoying the benefits of government backing and tax exemption, the National Savings Certificate (NSC) should be your option.

Starting with a small investment of Rs. 1,000 per month, with a lock-in period of five years, you can build a corpus of Rs. 17,338 on an invested amount of Rs. 12,000, earning 7.1% of returns.

The striking benefit of NSC is that the interest gets revised every quarter, and you can also avail of tax benefits of up to Rs. 1.5 lakh per annum. Thus, It is one of the most sought-after government schemes for shorter investment periods.

Post Office Monthly Savings Income (POMIS):

Even though this government-backed scheme doesn’t provide inflation-proof returns, it has been the top choice among the older generation due to its ability to offer a steady return of 7.1%, which is revised every quarter.

This 5-year lock-in saving scheme also provides tax benefits of up to 1.5 lakhs. With a single holder, you can save up to 9 lakhs, while with three joint holders, the maximum limit is 15 lakhs.

Sustainable Investments with SustVest

Sustainable investment is ideal for individuals seeking environmental and social returns in addition to financial gains, and the good news is that you won’t have to compromise on the financial aspect.

Starting with as low as 5000, this solar energy platform enables you to enjoy annual returns ranging from 10-15%, surpassing the returns offered by government-backed security and fixed deposits.

Moreover, there is no lock-in period for this investment. Additionally, you can also invest larger amounts of up to 25 lakhs with SustVest, allowing you to park your substantial savings. With more than 3000 investors this medium is becoming popular with millennials

Where We Can Invest Money: Moderate to High-Risk Options

When considering moderate to high-risk investment options, it’s essential to remember that higher risk also comes with the potential for higher returns. Here are a few investment avenues that typically fall into this category

Stock Market – High Risk

If you have financial expertise or trust someone with financial knowledge and have a higher risk appetite, investing in the stock market may be your calling due to the ample options available.

You can choose stocks with good past performances that align with your risk appetite. Additionally, you can select stocks from your preferred sector according to your goals, and you have the flexibility to start a Systematic Investment Plan (SIP) or invest a lump sum.

The returns in the stock market can vary widely, ranging from -10% to potentially 500%. It’s important to remember that higher risk also means lower returns when the market trend is unfavorable. However, the dynamic generations of today require additional income sources, and choosing the right stocks for the long run could provide just that.

Mutual Fund – Moderate And High Risk

Investing in a mutual fund is similar to sharing a load with others. By pooling resources, investors can access a diversified portfolio that spreads risk across multiple investments, reducing the impact of any single investment’s performance.

Whether you start a Systematic Investment Plan (SIP) with as little as 1000 rupees or make a lump sum investment of lakhs, mutual funds offer flexibility. You have the freedom to choose funds from your preferred sectors, such as energy, infrastructure, digital, green, or tax-saving schemes.

The returns in mutual funds, similar to the stock market, can vary significantly based on the type of funds you choose. Depending on the performance of the underlying investments, the returns can range from as low as 1% to as high as 60%

Alternative Investments: Higher Risks

Cryptocurrency

It has taken the world by storm with its highly volatile returns people have earned millions and lost millions it’s like walking on eggshells by investing in cryptocurrencies like Bitcoin, Ethereum, and many more.

Venture capital

Alternative investments like VC or investing in a startup come with a lot of potential. This form of investment can be rewarding but carries substantial risk, as many startups fail. Investors provide capital in exchange for equity and typically look for innovative businesses with the potential for significant returns.

NFT – Non-Fungible Tokens

NFTs are unique digital assets that represent ownership or proof of authenticity of a digital item, such as artwork, collectibles, or virtual real estate. NFTs have gained attention for their potential as a new asset class, but their value is highly speculative and can be subject to market trends and investor demand.

Smallcase

Investing in Smallcase is akin to investing in mutual funds but with greater control over your holdings. With Smallcase, you have the ownership of individual shares, and these shares are held in your demat account. This gives you direct ownership and transparency in the underlying stocks or securities of the Smallcase portfolio.

Smallcase has gained popularity among millennial investors due to its ability to compound interest and its inclination towards investing in unexplored yet potential ventures. It provides an avenue for investors to take calculated risks and tap into promising investment opportunities that may not be part of traditional mutual fund portfolios.

Where We Can Invest Money: The Final Verdict

An answer to where we can invest money goes beyond simply listing investment instruments. We also need to consider our individual circumstances, risk tolerance, and investment goals to provide personalized guidance. It’s true that not all investors constantly seek higher returns. At times, safety and security take precedence.

When planning for retirement or generating passive income, you may prioritize safety. However, it’s also important to note that there is a middle ground. SustVest, for example, offers an option that combines purpose-driven investing with safer yet higher returns compared to traditional instruments.

It’s vital to assess your risk tolerance and explore options that match your goals. Seeking professional advice can help in making informed decisions that strike the right balance between risk and potential returns.

Founder of Sustvest

Hardik completed his B.Tech from BITS Pilani. Keeping the current global scenario, the growth of renewable energy in mind, and people looking for investment opportunities in mind he founded SustVest ( formerly, Solar Grid X ) in 2018. This venture led him to achieve the ‘Emerging Fintech Talent of the Year in MENA region ‘ in October 2019.