2023 has something for each type of investor. Even though the world economy is crashing and people are losing jobs, investors know that they can make money even when there’s no money.

This article on 10 Best Investment Plan With High Returns In India 2023 will help you to understand these investment options better. If you are looking to diversify your investment with a mix of high, moderate, and low-risk investment plans, keep reading!

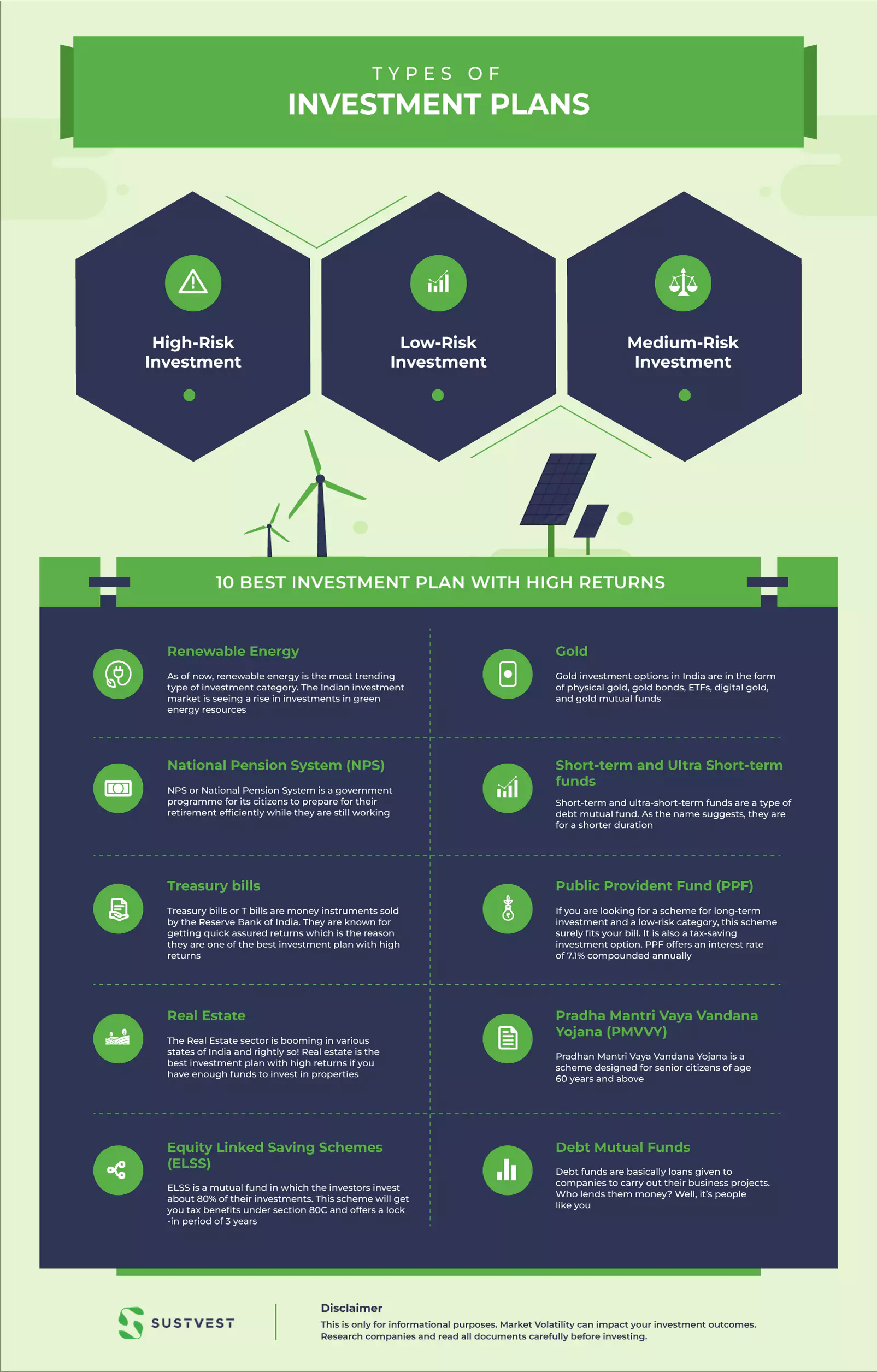

Let’s briefly discuss different types of investments based on risk factors.

Types Of Investment Plans

Every investment plan has its risks. Investors must be aware of those risks so they can be prepared to recover from them. Investment in share markets is the riskiest, but there are some alternatives to it. It is important to find the best investment plan with high returns that caters to your financial goals.

Before jumping to the best investment plans in India with high returns, here is a brief on high-risk, moderate-risk, and low-risk investments.

1. High-Risk Investment

These are the investment options that invest in equity or stock of the companies. They are in the high-risk category, but they are also considered investment plans with high returns.

Investors like to invest in them for a long-term period as the returns are well-paid at maturity. The income under them is taxable as per the STCG and LTCG.

This type of investment is not for people with a low-risk appetite.

Examples include real estate, Equity mutual funds, stocks, and share market investments, etc.

2. Low-Risk Investment

Low-risk investments are those investment options that invest in government securities like T bills, renewable energy assets, Sovereign bonds, NPS, NSC, PPF, PMVYY, etc.

They give good returns in lieu of the risk involved. Investors choose to invest in them because of fixed interest rates and tax benefits.

3. Medium-Risk Investment

Medium-risk investment options are sought after by investors who have a slightly aggressive taste in investment. They include debt mutual funds, short and ultra-short mutual funds, ELSS, etc.

The returns are higher than some investment forms but the risk can’t be ignored.

It is important to choose your options well. Now, let’s look at the investment options that will help you to make a decision.

10 Best Investment Plan With High Returns

We have curated a buffet of 10 investment plan with high returns. It includes traditional investment options like NPS, and GSB and then some alternative investment options like investing in renewable energy or green energy projects.

The investment plan discussed here varies in time duration. It includes short-term investment schemes that mature in just 3 to 6 months or a maximum of 3 years. And, the Long term investment schemes have a lock-in period of 15 years.

Starting with the first most sustainable investment option i.e. Renewable Energy. Let’s dive in the list of some of the best investment plans with high returns!

1. Renewable Energy

As of now, renewable energy is the most trending type of investment category. The Indian investment market is seeing a rise in investments in green energy resources. As per the world economic forum, the year 2021 saw a rise of 125% in renewable energy investment. In 2022, India has emerged as the 3rd most suitable place for renewable energy investments.

The reason for such growth is the shift from traditional energy-producing methods to new green energy alternatives. The government has taken initiatives to attract investors from all corners. Here are the categories of renewable energy which are backed by the government and are attracting investors.

- The solar sector is booming with investment as it has advanced in technology and has survived the initial phase. India is planning for 100,000 solar pump installations for agricultural lands.

- The government is investing in 100 smart city projects which will have rooftop solar and 10% use of renewable energy as the source. This is attracting investment from real estate, solar technologies, and other green energy sector companies.

- Next is the up-gradation and modernization of watermills and micro hydro projects. This sector again is attracting investment from green energy, energy storage options, the electrical sector, and infrastructure companies including real estate.

- Green energy corridor is promoted to create 12600 ckm of inter-state and intra-state transmission lines. Other than that, there are government schemes to involve investors to invest and take part in the green energy revolution.

Renewable energy assets have seen a rise in investments and returns and are considered to be one of the best high return investment in India. They offer a wide variety of investments with low risk and better ROI than regular traditional investments. You have the option to choose from monthly, quarterly, or annual interest payment schemes. Which is great! But, the only issue an investor may face is where to invest.

There are private companies in the green energy sector that help investors to invest in renewable energy projects. These companies work on various projects and have ties with the government and other private companies. They need financial assistance just like any other company. That’s where investors both big and small can contribute and earn a percentage of interest. One thing more, this is a tax-saving investment option.

SustVest is also one such company that works on solar energy projects, which is the fastest-growing renewable energy sector in India. Check out the projects to invest in here.

Check out our blog on ‘What Are The Different Solar Energy Finance Options In India’ here.

2. Gold

Gold investment options in India are in the form of physical gold, gold bonds, ETFs, digital gold, and gold mutual funds. Gold has always been considered an investment option in Indian households. They offer good interest return rates and are at low risk. The investment period depends on the type of gold you buy. Let’s see the pros and cons of each.

| Type of Gold Investment | Pros | Cons |

| Physical Gold | Can be bought in the form of jewellery, coins, bars, or bullion, in its original form. Readily available. Can be bought and sold at any time, with no locking period. Liquid investment. I gram of gold can be bought for INR 6000 or less depending upon the carrot price. Taxable under short-term and long-term capital gains. The gold coins issued by the government are available in 5, 10, and 15 grams weight. | Making charges up to 10%Storage locker charges up to 4% GST charges at 3% of purchase value Fear of theft, and purity issues. The long-term returns are very low. |

| Gold Mutual Fund | Can be bought in the form of jewellery, coins, bars or bullion, in its original form. Readily available. Can be bought and sold at any time, with no locking period. Liquid investment. I gram of gold can be bought for INR 6000 or less depending upon the carrot price. Taxable under short-term and long-term capital gains. The gold coins issued by the government are available in 5, 10, and 15 grams weight. | Returns depend on the market. An additional charge of 0.5 to 1 % is added to the price of purchased gold as an expense ratio. An additional charge between 0.1 to 0.2% is charged for managing gold by the banks. |

| Digital gold | The investment can be started by buying 1 gram of gold. The minimum investment is INR 1. Digital gold can be bought from Augmont Gold, MMTC and Safe Gold. The investment can be done directly from the app and is easily trackable. | Not regulated by any authority. GST at 3% is applicable on the price of purchased gold. The spread can expand up to 6%. |

| Gold Exchange Traded Funds (ETF) | The investment can be started by buying 1 gram of gold. The minimum investment is INR 1. Digital gold can be bought from Augmont Gold, MMTC, and Safe Gold. The investment can be done directly from the app and is easily trackable. | The minimum investment is INR 100. No making charges, storage, or purity issue. The spread is less. These are regulated by SEBI. Requires a DMAT account and app to invest in. |

| Sovereign Gold Bonds | The investor can earn high returns in less time. The share prices follow the gold-stock prices and gold mining companies stock prices. The minimum investment is INR 5,000. | Fear of discontinuation of the bond by the GOI. The interest earned at 2.5% is taxable as per the tax slab rates. If the bond was redeemed from the market, the interest earned is chargeable as per the short-term capital gains or long-term capital gains. |

Physical gold if bought in raw form meaning just as it is and not in any shape, you don’t have to pay any making charges on it. This will save you a lot of money.

Gold ETF and Gold mutual funds operate by investing in gold and in the stocks of the companies involved in gold mining. As a result, the volatility and returns of these two are the same.

From the above table, it is evident that Sovereign Gold Bonds are the safest gold investment options and are rightly on the list of the best investment options in India 2023.

3. National Pension System (NPS)

NPS or National Pension System is a government programme for its citizens to prepare for their retirement efficiently while they are still working. It is a safe option for investors who like to invest in long-term plans with low risk and comparatively steady returns.

NPS offers two investment models for investment. They are the Corporate model and the Public model. The Corporate model is for regular salaried employees and the Public model is for self-employed, freelancers, and other working class of the unorganized sector.

Let’s look at the scheme to understand its key features.

Who can invest in NPS? Any working individual can invest in this scheme to get its benefits. It is a highly recommended option of investment for those who fall under the 30% and above tax bracket in the income tax slab. That’s because NPS provides tax benefits as well.

- Age criteria: any individual citizen or NRI of the age of 18 to 60 years can invest in NPS.

- Under this scheme, the NPS investors are given a unique 12-digit code called Retirement Account Number (PRAN). PRAN allows the investors to access the two types of investment categories provided in this scheme: Tier I Account and Tier II Account.

- Tier I account has a locking period of up to the age of 60 years. Tax benefits are included with this account.

- Tier II account is like a normal investment account. You can invest the money, withdraw the returns, re-invest or do anything anytime. However, you don’t get tax benefits on this account.

- Minimum Investment amount at the time of opening the account: Tier 1 is INR 500 and Tier II is INR 1,000.

- The minimum Investment amount in a year is INR 6000 for tier I.

- Tier II account minimum contribution amount of INR 250 per contribution. And, there must be a balance of INR 2000 at the end of the year in a tier II account.

- There must be one contribution in a year in an NPS account.

- NPS is regulated by Pension Fund Regulatory and Development Authority (PFRDA), Point of Presence (POP), Central Recordkeeping Agency (CRA), and Annuity Service Providers (ASPs).

- You can subscribe to your NPS account by submitting the UOS S1 form to open a Permanent Retirement Account (PRA) along with the supporting KYC documents to Point of Presence-SP.

- For getting a Tier II account, you must have an active Tier I account. Then, submit the UOS-S10 form or Tier II activation form and PRAN Card to POP-SP.

- The cost to open an NPS account is INR 100.

- Withdrawal options include the following:

For Tier-I account: The investor must invest 40% of the accumulated savings to buy a life annuity. About 80% of that amount will be annuitized and the remaining can be withdrawn after resignation. In case of the account holder’s death, the complete amount will be given to the nominee.

For Tier-II account: the account holder is required to submit form UOS-S12 to the POP-SP. The fund collected in the NPS account depends on the NAV variation at the end of the day of requesting the withdrawal. Also, it can take up to 3 days to process the request and transfer the funds to the registered account in the CRA system.

4. Short-term and Ultra Short-term funds

Short-term and ultra-short-term funds are a type of debt mutual fund. As the name suggests, they are for a shorter duration. They are open-ended debt schemes.

The ultra short-term funds range from 3 to 6 months. While the short-term fund can be for up to 3 years. You can earn interest between 6% to 8% in just a period of 3 to 6 months. It is more than the FD interest rate.

These funds are known to invest in plans that give assured interest. That is why they are a low-risk option for investments.

Ultra short-term funds can be considered the best option to invest and earn a dividend on money that you aren’t going to use for 3 to 6 months. For example, you got a variable from your company, or you have saved up money for school fees or for buying any product. By investing that money you could earn interest. And after maturity, you can spend it too.

Banks like SBI, Axis, ICICI, Kotak Mahindra, HDFC, etc all have many ultra and short-term mutual fund schemes to invest in.

Before investing don’t forget to check the expense ratio and brokerage charges of the fund and choose wisely.

5. Treasury bills

Treasury bills or T bills are money instruments sold by the Reserve Bank of India. They are known for getting quick assured returns which is the reason they are one of the best investment plan with high returns. The risk involved is close to zero as they are backed by the government.

Now, T bills are issued by the government when it needs money for a period of less than 1 year. Also, these bills are issued at a discounted price.

The benefit you get with T bills is that at the time of maturity, you will receive the complete price value of the T bill and not the discounted price. The difference in the discounted price and the actual price will be your earning on that T bill at maturity.

Meaning, T bills are zero coupon securities. They do not provide any interest. And, the income earned from them is taxed under Short Term Capital gains.

There are three types of T bills issued by the RBI depending on the number of days it needs your money. They are 91 days, 182 days, and 365 days. The 91 days bill is auctioned every Wednesday. The 182 and 365 days bills are issued every second week of the month.

The investors participate in the auction and do the bidding. The lowest bid is considered the cut-off.

Earlier only big firms and businesses were allowed to invest in T bills. After 2016, they were opened to the public as well.

6. Public Provident Fund (PPF)

If you are looking for a scheme for long-term investment and a low-risk category, this scheme surely fits your bill. It is also a tax-saving investment option. PPF offers an interest rate of 7.1% compounded annually.

The tenure is of 15 plus 1 year, as the first fiscal year after opening the PPF account is counted as zero years. The tenure can be extended to 5 more years. The minimum amount you can deposit to open a PPF account is INR 500. The maximum deposit limit in a financial year is INR 1.5 lakhs.

For pre-mature closure, you must wait 5 years.

To get more details on PPF and other investment options head to our article on 7 best investment options in India.

7. Real Estate

The Real Estate sector is booming in various states of India and rightly so! Real estate is the best investment plan with high returns if you have enough funds to invest in properties. The rates of the properties are skyrocketing and are beyond the grasp of retail investors.

But, with REIT or Real Estate Investment Trust, you can also invest in various properties and become fractional owners.

REIT will invest your money in a variety of real estate projects. It can be of commercial, residential, or social importance. For example, shopping malls, hospitals, offices, residential societies, and other infrastructural projects.

Just like a mutual fund, you will invest a sum monthly in a project of your choice. The returns on it depend on the market. It also means that these are moderate to high-risk investments, depending upon the plan you have invested in.

8. Pradha Mantri Vaya Vandana Yojana (PMVVY)

Pradhan Mantri Vaya Vandana Yojana is a scheme designed for senior citizens of age 60 years and above. This policy is only for a 10-year period.

Here are some key features of this policy.

- The maximum investment limit is 15 lakhs.

- The return rate is between 7 % to 9% for 10 years.

- At the time of maturity, the principal amount is paid out, with the final pension and the purchase price.

- In case of the natural death of the policyholder, the amount will be returned to the successor/nominee/heir.

- At any moment, the pensioner can take a loan of up to 75% of the purchased price to aid in emergencies. The loan amount will be charged at interest and will be deducted from the pension at the time of its payment periodically.

- Modes of Pension Payment: NEFT, Aadhaar Enabled Payment System.

- The pension will be paid either monthly, quarterly, half-yearly, or annually to the pensioners as per the opted plan.

- The policy can be bought online and requires the following documents: an Aadhaar card, bank account details, PAN card, age proof, address proof, income proof, and retirement proof.

For more details on this policy head to the article Top 9 Fixed Income Investments In India.

9. Equity Linked Saving Schemes (ELSS)

ELSS is a mutual fund in which the investors invest about 80% of their investments. This scheme will get you tax benefits under section 80C and offers a lock-in period of 3 years.

ELSS investments are prone to market volatility just like any other mutual fund. But, the returns are comparatively high and compensate for any fluctuation that happened in the share market price.

ELSS offers the shortest investment locking period compared to NSC, saving bonds, etc. You can withdraw your returns after completing 36 months of taking the ELSS scheme.

As recommended by many experienced investors, the best way to invest in an ELSS fund is to go with a SIP. this will give regulated growth and help in getting better long-term returns.

Now, to invest in ELSS you can use any platform or application available online. Search for the ELSS mutual funds, and a variety of funds will appear.

The tricky part is to select the right ELSS mutual fund. For that, look at the portfolio of each and see their returns for at least the last 10 years.

The second thing to look for is how diverse their investment is, and what kind of company they invest in. The more diverse the portfolio, the lesser the risk.

The third thing to look for is whether their scheme is covered under ELSS and shows tax benefits.

Some examples of ELSS mutual funds are Axis long-term investment scheme, IDFC tax saving fund, Meera trust fund, etc.

ELSS is considered as one of the best plans for high returns on investment if the right investment decisions are made at the right time. Well, it’s the same for all stock investments.

10. Debt Mutual Funds

Debt funds are basically loans given to companies to carry out their business projects. Who lends them money? Well, it’s people like you. The public and private companies sanction bills and bonds to be bought by the investors. The investors get an interest on the bonds and bills purchased.

The investor receives earnings every month in the form of installments. Now, the bonds can have both fixed and floating installments. There are a total of 18 types of bonds in the market. Therefore, choose wisely!

The fixed income debt funds have a fixed monthly installment, these are also called fixed-income security funds. You know the interest and percentage you will gain on maturity.

It’s true that debt funds offer more returns than FDs and Post Office schemes, but they are subjected to market conditions. A few examples of types of debt funds are corporate funds, government bonds, treasury bills, and money market instruments. With proper research, you can select the best investment plan with high returns among the debt fund options in the market.

FAQs:10 Best Investment Plan With High Returns In India 2023

How is an investment in solar energy plants the best investment plan with high returns?

Direct investment in solar energy plants is one of the best investment plan with high returns in 2023. With SustVest you can choose to invest in solar projects from the list of available projects. You can begin investing with an investment of as low as INR 5000

What are some of the best investment plan with high returns in India?

Some of the best investment plan with highest return in India in 2023 are:

- Equity funds

- Renewable energy investments

- Real estate

- Gold

- Mutual funds

Where should you invest your money?

How risk appetite affects your investment choices, plays a very important role in picking an investment option. Here is a list diversified options to keep in mind.

1. Equity Mutual Funds: Long-term growth potential.

2. Fixed Deposits (FDs): Stable, low risk returns.

3. PPF & NPS: Tax-efficient, retirement-focused.

4. Real Estate & Gold: Diversify your investments.

5. Sustainable Choices: ESG Funds, Green Bonds, Renewable Energy Stocks, Sustainable Startups.

Conclusion

Alright, that was all about the 10 Best Investment Plan With High Returns In India 2023. Whether you are looking for short term or long term investment plans with high returns, it can’t be ignored that your investment should encourage sustainable investments. Sustainable investment options like renewable energy assets, solar projects, etc not only have withstood the volatile market but are also good for the environment.

As an alternative source of passive income, everyone is looking for opportunities that are viable and have a long-term hold on profits. 2023 is expected to be the best time to invest in green energy. Don’t feel left out, SustVest can help you join the race in no time. Invest in solar energy projects with the best investment plan and high returns now!

Founder of Sustvest

Hardik completed his B.Tech from BITS Pilani. Keeping the current global scenario, the growth of renewable energy in mind, and people looking for investment opportunities in mind he founded SustVest ( formerly, Solar Grid X ) in 2018. This venture led him to achieve the ‘Emerging Fintech Talent of the Year in MENA region ‘ in October 2019.